Overview

Seylan Bank (SEYB) was incorporated in 1987 and obtained a listing for its ordinary shares on the Colombo bourse in 1989. Today the bank stands as the 4th largest private commercial bank in Sri Lanka with an asset base of LKR142.9 bn whilst operating an island wide branch network of 94. Today the bank is recovering from the crisis situation under the new management and the bank has potential for upside (along with the expected industry upside) given the bank will return to its normal operating levels by end of 2010.

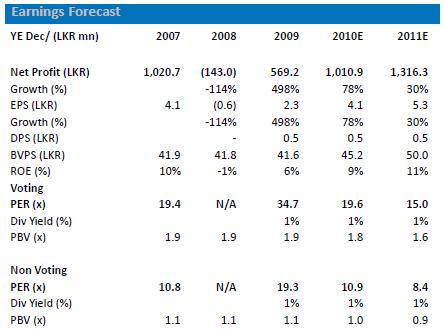

SEYB’s net profit has grown by 66% YoY to LKR311.8 mn in 2Q2010 enabling cumulative 1H2010 earnings to grow by 169.8% YoY to LKR507.3 mn. Net profit growth during the quarter was mainly on the back of 37% YoY increase in net interest income and 29% YoY reduction in provisioning cost. With the expected economic growth the loan growth expected to gather momentum from 2H2010 onwards coupled with improving asset quality and healthy capitalization levels banking sector outlook remains positive. SEYB’s net interest margins are expected to be intact at around 5%, whilst continuing to benefit from an island wide branch network. We are revising up our forecast 2010E net profit at LKR1,010.9 mn (up 78% YoY) and projected 2011E net earnings to LKR1,316.3 mn (up 30% YoY). Thus the voting share is trading on

19.6x forecasted 2010E net profit and 15.0x projected 2011E net earnings, 1.8X PBV. The non voting share is attractive on 10.9x forecast 2010E net profit, 8.4x projected 2011E net earnings and 1.0x PBV .

SEYB’s interest income has dropped by 20.9% YoY to LKR4,204.1 mn largely due to the high non performing loans and low interest rates but on the contrary SEYB’s interest expenses have dipped by 43.2% YoY to LKR2,183.0 mn which has weathered the negative impact on interest income enabling the bank to improve their NII.

Bank’s OPEX has increased by 4.3% YoY mainly on the back of a 8.1% YoY increase in personnel expenses whilst all other expenses have been kept in check. Further it is also encouraging to see during 1H2010 banks OPEX has reduced by 1.8% YoY which has helped the cost/income ratio to come down to 66%.

Improved NII levels and marginal increase in OPEX have helped the bank to record a growth of 112.8% YoY to LKR893.9 mn in 2Q2010.

Provisioning cost has reduced by 29.2% YoY to LKR167.7 mn in 2Q2010 mainly due to 10.8% YoY reduction in specific to LKR360.9 mn and 90.8% YoY improvement in recoveries to LKR202.0 mn.

Value added tax on financial services has increased by 158.1% YoY to LKR189.0 mn and corporate tax has increased by 106.7% YoY to LKR193.4 mn which in turn has increased the total tax bill. Effective tax rate as at 30th June stood at 56%.

Bank’s bottom line has grown by 66.0% YoY to LKR311.8 mn mainly on the back of improved NII and reduction in provisioning costs despite increase in total tax bill and marginal increase in OPEX. Banks cumulative 1H2010 earnings have grown 169.8% to LKR507.3.

Bank managed to reduce its non performing loans by 2.5% YoY to LKR27.5 bn during the quarter. Thus gross NPL ratio has witnessed a considerable improvement to 25.6% in 2Q2010 from 29.3% in December 2009 and Net NPL ratio improved to 18.4% from 22.3%. However compared to the industry average of circa 8% SEYB’s NPL ratios are still at high levels.

SEYB’s loan book has recorded a 2.2% YoY growth in 2Q2010 to LKR64.1 bn where we saw the private sector credit growth (2.2% YoY growth in May)picking up during the 2Q2010.

Deposit base grew by 1.1% to LKR107.0 bn during 2Q2010 mainly due to growth in savings and demand deposits. Further we see a shift in the deposit mix towards low cost CASA deposits which will help SEYB to reduce it funding costs.

SEYB is showing signs of recovery from the financial turmoil which it underwent in 2008. Therefore on the back of the bank’s recovery, favourable macro economic environment coupled with expected credit growth in 2H2010 and growth potential for the banking sector we forecast 2010E net profit to rise by 78% YoY to LKR1,010.9 mn.

The voting share currently trades at 19.6x projected 2010E earnings and 15.0x on projected 2011E earnings whilst trading at 1.8x PBV. The voting share is trading at near 50% premium to the sector, however given SEYB’s branch network and reach and the recovery in its core business that we have seen during 1H2010 coupled with the reviving macro economy and growth potential in the banking sector SEYB.N. has further upside, hence we rate SEYB.N a HOLD

The non voting share is attractive at 10.9x projected 2010E earnings and 8.4x on projected 2011E earnings whilst trading at 1.0x PBV. The non voting share trades near 44% discount to the voting share where the normal discount between the voting and non voting share in the banking sector is 25-30%. Therefore we believe the gap between SEYB.N and SEYB.X should narrow in the future and given SEYB’s recovery in its core business that we have seen during 1H2010 coupled with the reviving macro economy and growth potential in the banking sector we rate SEYB.X a BUY

0 comments:

Post a Comment